The following is a LinkedIn Article written by Carl Christian Rösiö, Principal at Euclid Transactional.

Q4 2025 closed with clear momentum in the EMEA and APAC transactional risk markets, bringing an end to a record year for Euclid in EMEA and APAC. We saw higher submission volumes and larger average enterprise values. In a market where processes are moving quickly, brokers and clients are prioritizing responsive underwriting, clear positions on key terms, and policies that respond when claims hit.

Here’s what stood out:

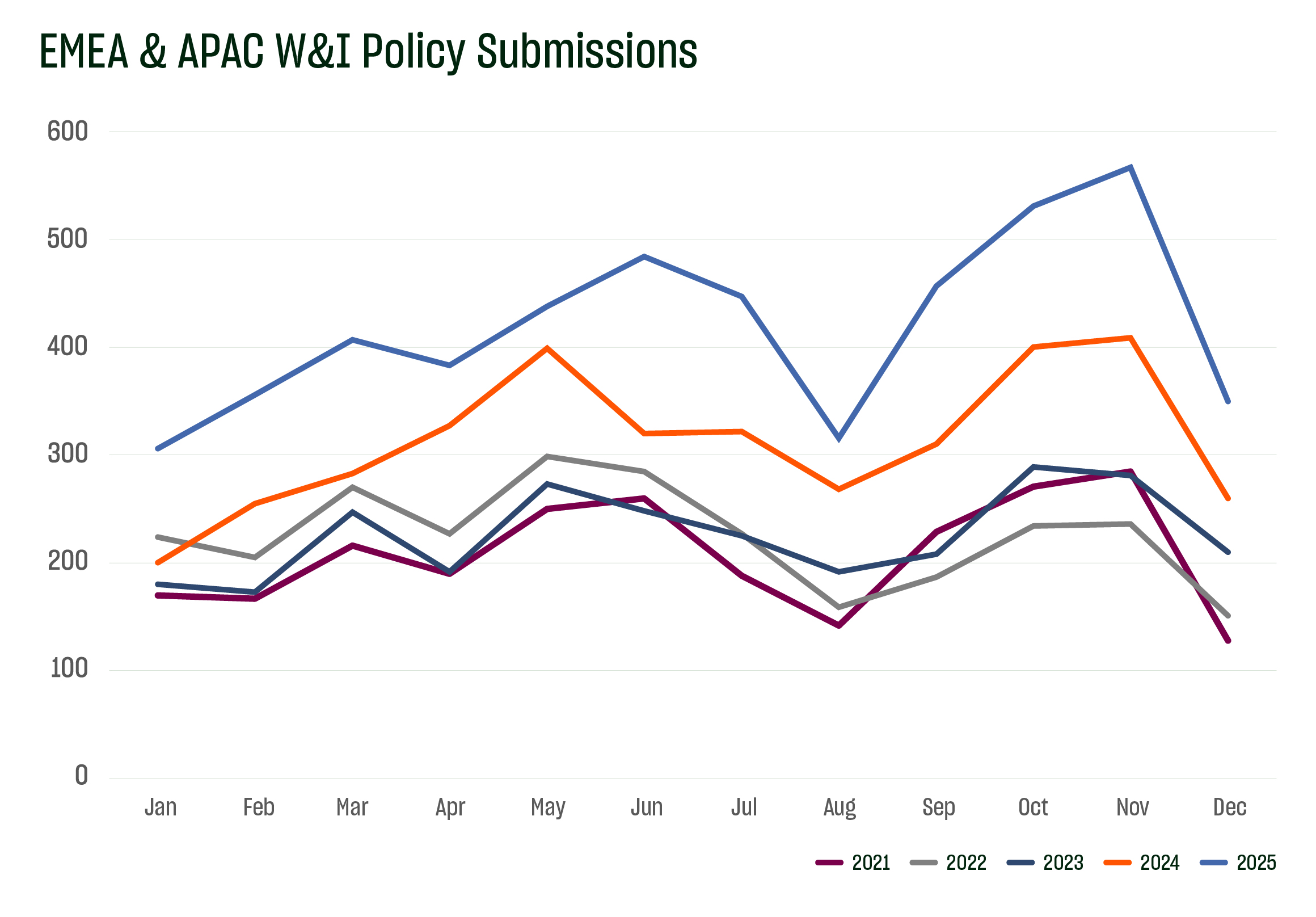

- In Q4, Euclid Transactional received 1448 EMEA and APAC W&I submissions, our highest Q4 on record, up 36% from 2024.

- In 2025, submissions increased in Real Estate (+58%), Healthcare (+157%), and Financial Services (+50%), while volumes declined in Retail (-15%) and Entertainment & Media (-18%).

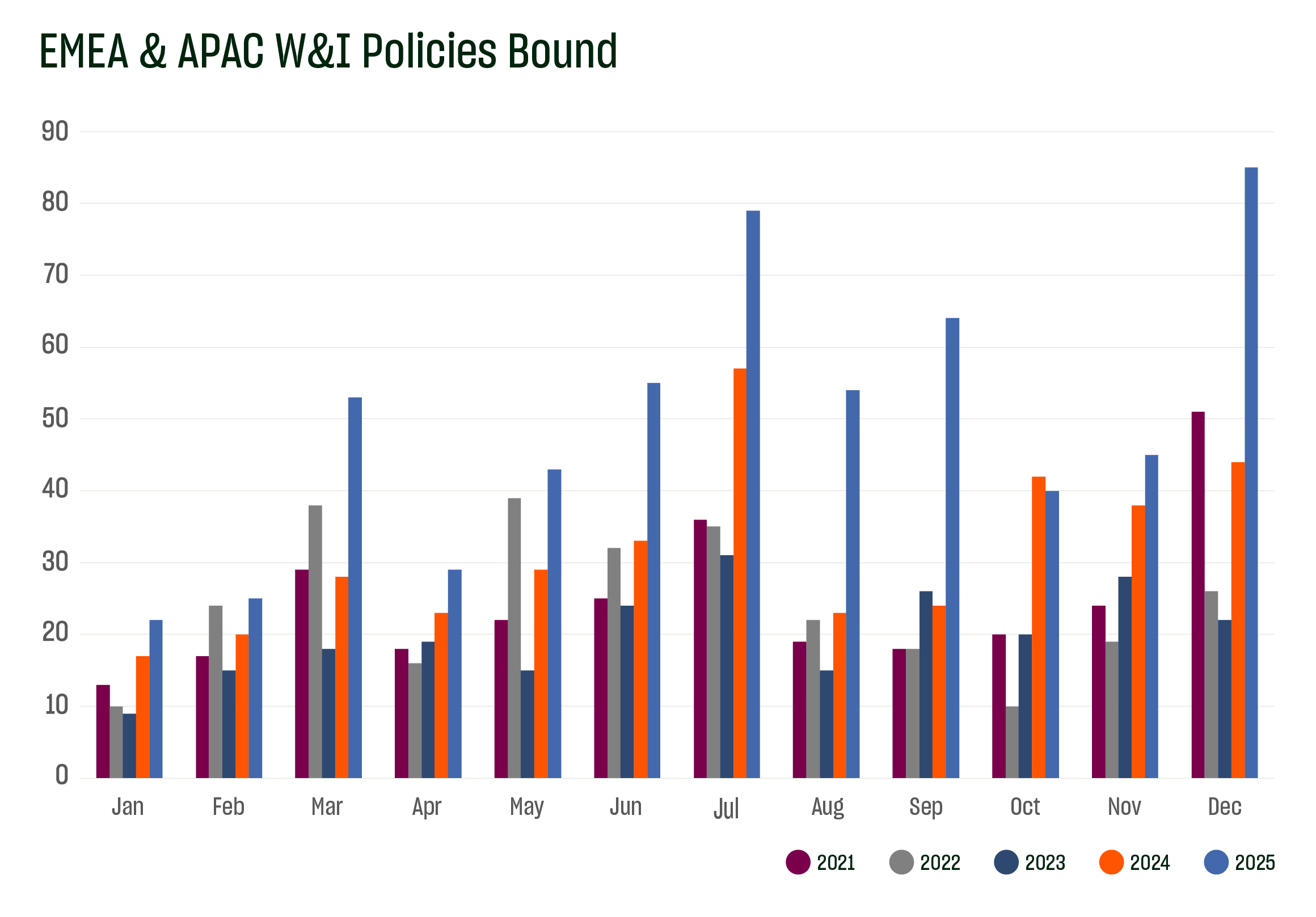

- We bound 170 policies in Q4 2025, a 37% increase year over year. December alone accounted for 85 bound deals, marking our highest monthly total on record.

- The average enterprise value in Q4 reached $381 million, reflecting a strong inflow of large deals into the market. We also saw a significant rise in submissions for W&I deals over $1 billion, which were up 45% in the quarter.

- Our APAC region showed particularly strong momentum, with 254 submissions received in Q4.

We proudly announced earlier this year that we eclipsed $1 billion in RWI / W&I claims paid in less than 9 years of operation. In 2025, our carriers paid a further $463M in claims as a result of 67 payments. Our 2024 Global RWI Claims Study highlights the increasing severity of loss payments, underscoring the urgent need for meaningful and lasting upward rate movement.

Euclid Transactional remains focused on increasing and maintaining sustainable W&I rates on line to continue to deliver the exceptional underwriting service and fair and efficient claims process for which we are known. With broader indicators pointing to a stronger M&A environment heading into 2026, we expect continued demand for transactional solutions.

What are you seeing in EMEA and APAC right now – timelines, pricing, exclusions, and appetite for larger deals? Let’s discuss.